[For up-to-date information on the state of IR35, take a look at IR35 For Contractors and Hiring Businesses: What You Need to Know]

IR35 is the regualution which is due to come into effect and will impact the engagement of contractors via Limited Companies or Personal Service Companies (PSCs). It was due to land in April 2020, but because of the implications from Covid-19, this has been delayed until April 2021.

(As this remains in an ongoing discussion, we have noted some updates from throughout 2020 at the bottom of this article)

Historically, responsibility for determining the employment status of an engagement fell to the individual contractor, together with liability for correct payment of associated PAYE taxes. Going forward, responsibility for determining the employment status of engagement will rest with the hiring company, and liability for the appropriate deduction of PAYE taxes will rest with the entity paying the contractor.

With this being such a large consideration for employers and contract employees alike, we hosted a panel session to give clients and contractors expert views on the forthcoming changes to legislation governing the engagement of "off-payroll" workers and contractors. We were joined by Oliver Weiss, Partner at Blake Morgan LLP, Catherine Hearn, Director of Resourcing & Talent at BBC, and Rob Woodward, Associate Director Employment Tax at BDO UK LLP.

In summary

Summarising the proposed changes, Oliver Weiss explained that the only difference was that it now becomes the hiring entity (or client) who is responsible for determining the employment status of the assignment, rather than the self-employed contractor or Personal Service Company (PSC). This place a duty of care on clients to ensure that the work they commission is correctly treated for tax purposes, with appropriate income tax and PAYE deductions being made at source. Liability for correct tax deductions in line with the status determination rests with whoever is paying the worker (either the client or agency if not engaged directly).

Having already come into effect across the public sector in 2017, the challenges and controversy over these changes have been well documented, and many clients and contractors fear a significant impact to the way that they work.

Supporters of the planned changes point to potentially unfair tax advantages enjoyed by PSC contractors who really should be regarded as employees, while critics consider the changes as a curtailment on the activities of the genuinely self-employed. In recent weeks increasing criticism has been levied at HMRC for potentially creating “zero rights” employment status for millions of people, who will be regarded as employees only for tax, but share in few, if any, of the usual benefits associated with formal employment.

The panel of experts was quick to agree that open, transparent and constructive communication was vital in ensuring that accurate status determinations supported contract work.

Evidence shows that hiring entities broadly fall into three distinct groups: those that have little or no awareness of the planned changes, those who have resolved at the outset to issue a blanket "inside IR35" status determinations, and those who take a considered and personal view of each decision. The latter group were by far the best placed to ensure that they were prepared come April 6th.

Catharine Hearn explained that trying to take shortcuts or resorting to “blanket determinations” risked undermining trust and relationships with contractors that could make a long time to rebuild. Instead, she urged clients to be pragmatic and open– remembering always that there was a human at the end of each decision, whose work and livelihood was in consideration.

Making an accurate employment status determination:

Rob Woodward noted that for decades lawyers, policymakers, businesses, and contractors have grappled with how to accurately and consistently define the employment status of a worker. The reality is that there are considerable ambiguity and nuance, making it essential to. The following steps were suggested to help hiring managers make appropriate determinations:

Consider using the HMRC Check Employment Status Tool (CEST). Far from perfect - and much maligned in the press in recent months - this tool does at least structure a set of questions to help guide clients towards a reasonable determination.

There is no legal obligation to use CEST, and many alternative tools and services have been developed by employment advisory and legal professionals. Clients must be able to demonstrate that they have exercised “due care” in reaching a status determination.

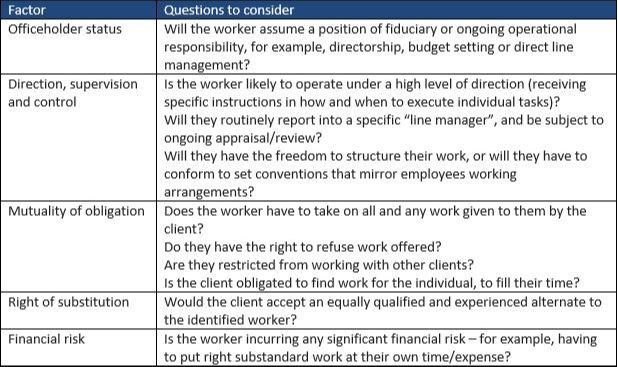

Consider the critical determining factors carefully. These are simplified in the table below:

Engage in dialogue with the contractor or agency early in the process. There may be budget implications of engaging "inside" or "outside" IR35, and this may influence how you want to frame the project.

Avoid surprises. Make sure that everyone knows and agrees with the status of an assignment well in advance of an assignment commencing.

Document your decision and any supporting evidence or tools that helped you get there. This will aid future status determinations and ensure that all parties have clarity should a determination be challenged later.

If you determine work to fall "outside" IR35:

Many of the strategic projects we support clients on have already been determined by clients to fall outside of IR35. In these instances, clients are free to continue to engage contractors on a PSC - limited company - basis. There will be no change to any of these engagements.

If you determine work to fall "inside" IR35:

Where you determine that the practice constitutes temporary employment, any contractor will need to be engaged on a PAYE basis. As a client, this means that you will incur the additional costs of Employers National Insurance contributions and holiday pay for that worker.

Contractors may also seek to renegotiate their rate if they are engaged on a PAYE basis.

What this means for your Freshminds projects

The vast majority of Freshminds projects won’t be affected by the changes. At the junior end of our service offering, all contractors are already engaged on a PAYE basis, and this will continue unchanged.

At the senior and specialist end, the majority of our clients engage us on a consultancy agreement – under which we deliver outcomes against an agreed statement of work. Any subsequent employment status determination and PAYE tax liability relating to individuals engaged on that project rests with Freshminds. Again, this will remain unchanged.

Where a client wishes to engage a contractor directly, and determines this engagement to sit inside IR35, we will process all payments through our PAYE payroll. This may have an impact on your project cost, as additional employment costs may apply, and some contactors may adjust the rates at which they are prepared to work.

With an unrivalled global consulting network we are confident of consistently and compliantly delivering excellence on demand, supporting our client’s deliver critical strategic and commercial projects.

Updates from 2020

MPs voted to approve the 2021 rollout (delayed from 2020), but there are still powerful voices calling for the delay to be extended to 2023. With a large majority, the government has moved forward with the legislation.

The approved legislation did, however, include a wording error, which HMRC have acknowledged and are working to resolve. Although quite technical, it really highlights what a complex area this is, and, of course, those opposed to the rollout have hailed this as evidence that the legislation is "half baked" and should be scrapped. Although it most likely won't be.

Should the government continue to extend substantial financial support to businesses beyond March 2021 (very likely if we are still in a position of economic lock-down), it may be possible that they will push back the rollout, but generally considered unlikely. Best case would probably be an introduction of the new rules, but a deferment for up to 12 months on payment, giving PSC contractors time to get their cash-flow in order, or find a PAYE job.

The move to extend a version of the JSS to self-employed and limited company contractors earlier in the year was done with the clear instruction from the Chancellor - everyone should be supported, and everyone should pay their share.

Got questions about how IR35 applies to you? Check out our FAQS for understanding IR35.